Finance Friday: Are you influential?

Finance Friday: Are you influential?

Starts with getting everyone on the same page

Photo: Matthew Needham

I wrote a post on Linkedin this week.

It got a lot of attention and a lot of new subscribers have joined this Substack as a result.

So thank you, and welcome to the CFO Partner. It’s great to have you here!

If you’re keen to find out more about the CFO Partner and what we have planned for 2024 - you can check that post out here.

Influence

The holy grail for the CFO and every Finance team.

I’ve been thinking a lot about influence this week.

Mainly because I have an upcoming workshop on it soon, but also because you need it to create more impact in your work:

I believe that in order to create impact, you need to be influential.

Being more influential with our executive teams, our boards or our stakeholders is what we all seek.

In many ways, it’s like the ocean tide.

It ebbs and flows.

Sometimes you’re influential.

And sometimes you’re not.

Sometimes you’re influential about some things.

And sometimes you’re not.

Trust

Although Influence and trust are related.

Influence isn’t quite the same as trust.

Trust is more binary.

You either have it,

Or you don’t.

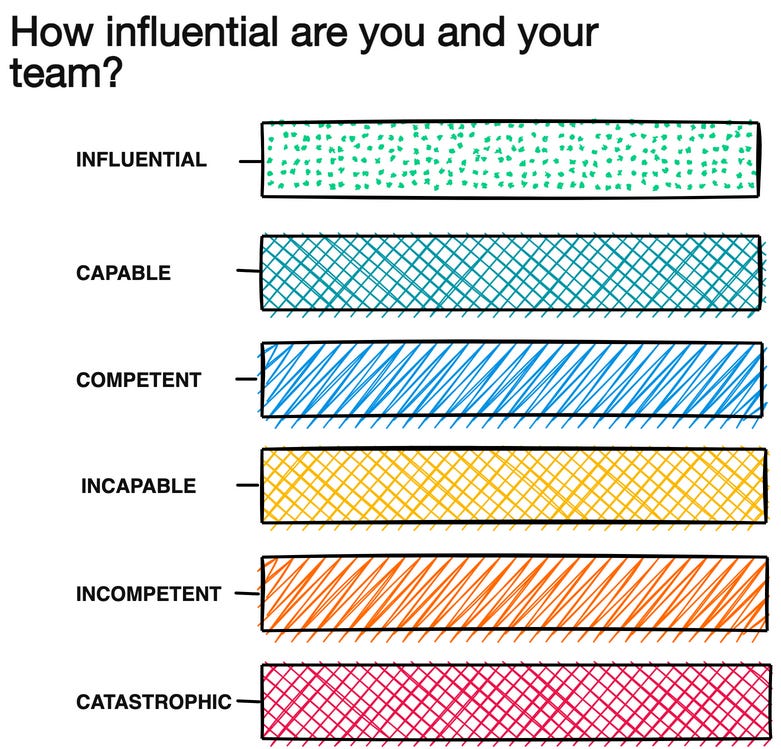

Nuance of influence

Influence is more nuanced.

This week I built a model around it to describe it better.

By asking the question:

Let’s start in the middle.

Competent to Influential

Assuming you’re doing a good job, getting the basics right, but not much time for adding value;

I’d describe you/your team as competent.

Nothing wrong with that. That’s ok.

If you’re able to do the basics right, have capacity for consistently adding value, then you’re capable.

But if you’re truly partnering, provided actionable, insightful advice, being actively sought out for your opinions, then you’re influencing.

Competence to Catastrophe

But, if on the other hand you’re short of resources, a person down or simply workload squeeze, such as year end/budget then you’re incapable.

It’s not that you can’t do the job, you’re incapable of doing it because there’s no one there to do it.

It could be temporary. Or it could be over an extended period of time.

But, when you’re incapable and someone leaves';

That makes you very vulnerable and the risk of making mistakes is high.

When you’re making mistakes, you’re seen by your stakeholders as incompetent.

If you make enough mistakes or make the wrong decision (or someone else does) based on incorrect analysis.

Then it could be catastrophic for you/your team and the organisation.

Whilst it can take time (a few months) to get from competent to influencing.

Getting from competent to catastrophic can happen very quickly.

The other think I find is that when you slip below competent, it can be difficult to recover, especially if you’re without key people or resources for more than a couple of weeks.

So what do you do about it?

The first step is to get every one on the same page.

And agree priorities.

The second step is to create capacity.

Finance teams spend too much time on low value work.

Teams need to free time and then manage the diary better.

This essentially boils down to 3 steps:

1. Understand where the time goes

2. Reduce or eliminate low value adding activities

3. Block time to work on priorities

Whilst tracking where times goes, you don’t need to account for hour and where it’s gone.’

Tracking time involves tracking where the time is going.

You don’t need to get all fancy and install time tracking software.

Use Excel.

Once you’ve collected all the time from everyone in the team, sit down and then look at where large amounts of time are spent on low value activity.

Then it requires dedicated the time to tackling it.

That means using the 4 D’s framework

Do it now

Decide when to do it or what to do about it

Delegate it, by transferring the task to someone with capacity or at the appropriate skill level

Delete it - stop doing it.

I think a good and fair target to aim for each week is eliminating 5% of the low value activity.

Then over about 6 months you should have eliminated it all.

The beauty is:

The gains don’t come in 6 months time though.

They come with the freed up time each week.

If 50% of a week is low/no value add - that’s around 20 hours a week.

Saving 5% would save you around an hour.

Of course, the multiplier effect comes into play.

That’s 1 hour per person impacted by the low/no value process.

In a team of 40, that’s the equivalent of an extra person.

In a few weeks, it would be like having an extra team.

Imagine that.

But it all starts with setting priorities.

Start of a new year - are the priorities clear for the next 3 months?

Are they widely understood?

If you’d like help setting/agreeing priorities for your team this year, and getting everyone on the same pages, please get in touch.

📢 This newsletter is brought to you by Matthew Needham Consulting - Helping CFOs and Finance Teams create more impact in their work. To find out how I can help or enquire about working with me, click here. 📢

Inspired by the idea of delegation, and keen to get advice on delegate tasks when previous precedents were there, to avoid being seen as pushing away of your responsibilities.